Disability insurance 101: What every resident needs to know

Fact checked by Mindy Valcarcel, MS

As a resident, chances are you have several types of insurance for the valuable things in your life, including health, house/apartment and car.

But many residents do not take the necessary steps to protect their most important and hardest-won asset — their ability to earn income to support themselves and their families.

I am a disabled physician who sustained a career-ending injury and am no longer able to practice OB/GYN. I learned a lot the hard way about disability insurance, and my mission is to share my expertise with fellow physicians to help you avoid the mistakes I made.

Above all, you need to be sure that your private disability insurance policy is written specifically for you, to cover the type of medicine you were educated and trained to practice. This article is the result of thousands of conversations with physicians like you. It covers all you need to know before you speak with a broker to protect your income and peace of mind.

What is disability insurance?

Disability insurance is income protection. It covers a portion of your income if you can no longer perform your job due to an illness or injury. It provides you and your loved ones with financial peace of mind during a time when finances should be the least of your worries.

Why is disability insurance important for residents?

As a resident, your livelihood and career depend on your performance of specific tasks/skills to deliver care and service to your patients. An injury or illness can severely affect your job performance. It can also have a major impact far beyond your job, on your personal life as a spouse, parent, athlete, etc.

As a resident, you may think disability will never happen to you. Cancer and other illnesses do not discriminate. Accidents are called accidents for a reason.

A short-term or long-term injury or illness could jeopardize your ability to cover basic financial needs for you and your family. Consider how long your savings would last if you ended up in this unfortunate situation. What if your last paycheck was really your last paycheck?

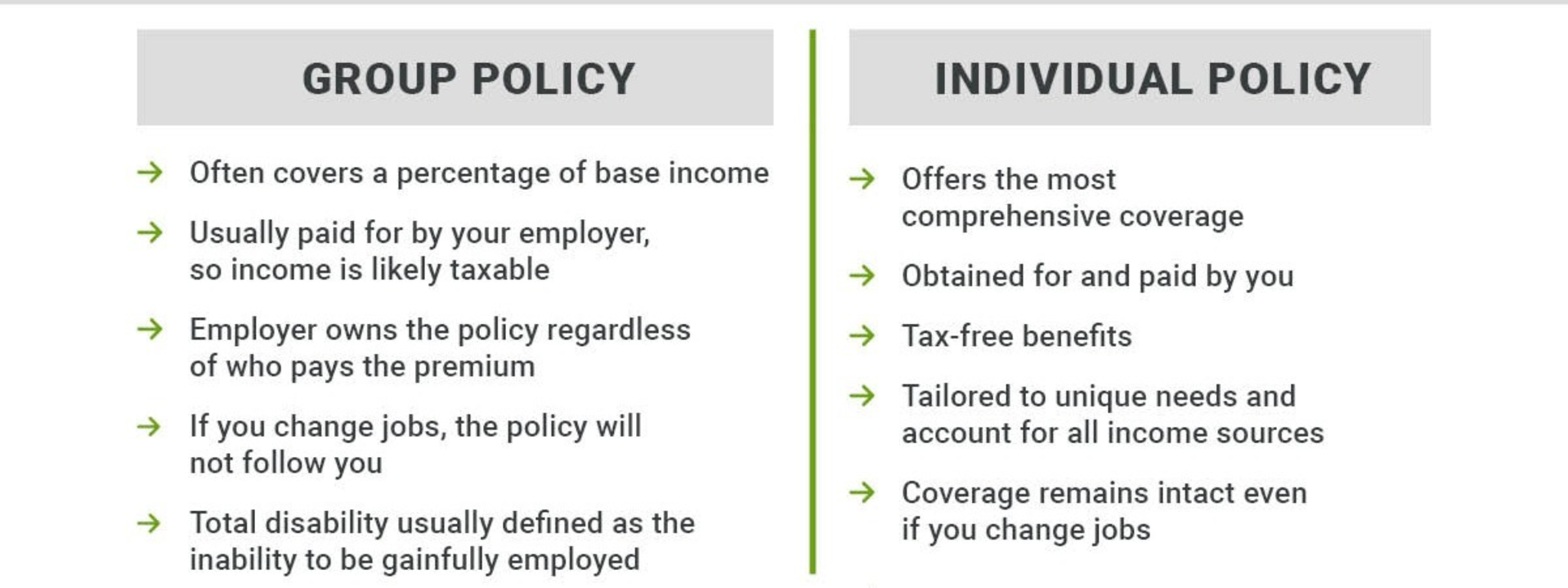

What is the difference between group and individual private disability insurance?

As a physician, there are two main types of disability insurance you need to know: group and individual long-term policies.

Group long-term policies are employer or association (like the AMA) policies. Employer policies are often paid for by your employer (some are voluntary), and it is one line on your open-enrollment plan. These policies often cover a percentage of your base income to a maximum monthly benefit that may be much less than you actually make.

Individual private long-term policies are obtained for and paid by you. They offer the most comprehensive coverage. As with all insurance plans, the riders, or building blocks, are the most important part of the policy.

Group long-term insurance provides some coverage depending on your situation, but you should not rely on it as your sole means of income protection because there are some major limitations.

If your employer pays for the policy, any income you receive is considered taxable, which will decrease the true amount that you bring home. The exception is if they treat the premium as imputed income.

For group policies, whether your employer pays the premium or you pay the premium, your employer owns the policy. They create it, they control it and, more often than not, they keep it. Most policies are employment-dependent. If you change jobs, the policy will not follow you. It is not portable.

The definitions of own occupation and total disability may not be what you think they are. Your employer may say that their policy is own occupation, but look at the fine print. Most policies will define own occupation as what is held by the national economy or the local labor market. It is not what one employee does at one employer site. Many policies will limit the own occupation definition for 1 to 2 years, and then switch to any occupation. Additionally, most will define total disability as the inability to do your job AND not be gainfully employed. The gold standard for individual policies defines total disability as the inability to do your job (what you do day in and day out), regardless of whether you are gainfully employed in another occupation.

On the other hand, a quality private individual disability policy is specifically tailored to your unique needs and takes into account all sources of income. The benefits are tax-free because you pay with post-tax dollars. The policy is portable. You take it with you wherever your career takes you. The policy ensures your coverage remains intact even if you change jobs. It has the strongest language available.

Read the rest of the article on Healio.