Term vs. whole life insurance: What physicians need to know

by: Chirag P. Shah, MD, MPH; and Jayanth Sridhar, MD

Key takeaways:

Term life insurance is less expensive and can protect one’s family by covering liabilities and lost income.

Whole life insurance may be helpful for very high-net-worth individuals or parents with lifelong dependent children.

Physicians are often targeted by financial advisors promoting whole life insurance — advertised as a two-in-one solution for protection and investment.

This may sound appealing, especially to busy professionals with high incomes, but a closer look reveals that term life insurance is usually the more cost-effective choice for most physicians.

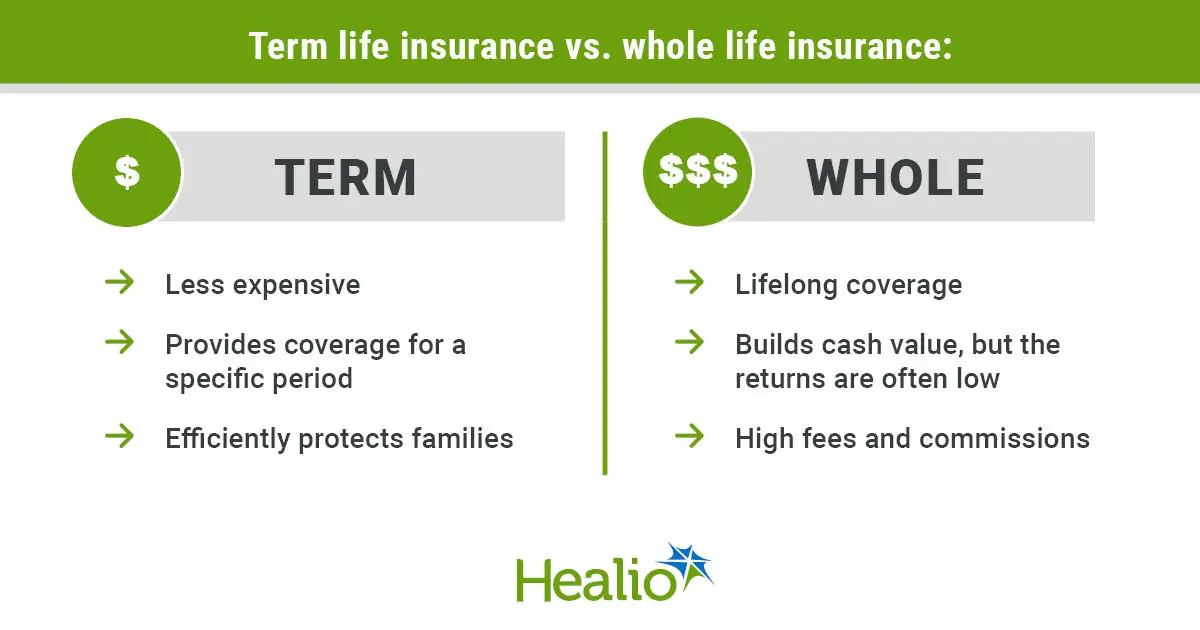

What is term and whole life insurance?

Term and whole life insurance are two common types of life insurance policies. Term life insurance provides coverage for a specific period (eg, 10, 20 or 30 years) and pays a death benefit only if the insured dies during that term — making it generally more affordable. Whole life insurance, however, provides lifelong coverage and includes a savings or investment component that builds “cash value” over time, but it comes with significantly higher premiums. The cash value grows at a low, fixed, tax-deferred interest rate, and eventually you can take out loans against your policy. These loans are deducted from the payout upon your death. It can take 10 to 15 years to build up enough cash value from which to borrow against, because much of your initial premium payments cover fees and commissions.

Simple protection at a lower cost

Term life insurance is designed to do one thing well: provide financial protection for a fixed period at a fraction of the cost of whole life insurance.

For most people, the primary goal of life insurance is to ensure that their families are protected against liabilities, such as a mortgage, student loans and/or college expenses, in the event of the untimely passing of the family’s breadwinner. Further, term life insurance can protect the family against the loss of the breadwinner’s future unrealized income. Term coverage accomplishes this efficiently, allowing one to redirect the large difference in premiums between term and whole life insurance toward more productive investments, such as a total stock market index fund.

One consideration is to purchase several term life insurance policies, each with varying duration. For example, one could purchase three $1 million policies at terms of 10, 20 and 30 years. Thus, one has $3 million of coverage for the first 10 years of coverage, $2 million for the next 10 years and $1 million for the final 10 years. This tapering coverage is hopefully inversely proportional to one’s growing portfolio, and directly proportional to one’s shrinking liabilities.

Whole life insurance: Pros and cons

Whole life insurance policies build cash value with tax-deferred growth. However, the returns on these policies tend to be low (often in the range of 1%-3.5% annually) and are diminished by high upfront administrative fees and commissions. Thus, it can take many years to accumulate enough cash value from which to borrow.

However, whole life insurance might be a valuable component of estate planning for high-net-worth individuals who have already maximized other tax-deferred investment vehicles, or for those with lifelong dependent children (eg, due to disability).

Beware of conflict of interest

Brokers earn significantly higher commissions selling whole life insurance policies, which can create a misalignment of incentives. It is not uncommon for physicians to be urged to buy coverage far in excess of their actual needs, or a broker to describe these policies as essential components of a solid financial plan when they might not be. A fiduciary financial advisor — one legally obligated to act in your best interest — can help give you unbiased advice.

Term vs. whole life?

Life insurance often becomes important when one has a family and liabilities. For most physicians, particularly those early in their careers, inexpensive term life insurance can protect one’s family by covering liabilities and future unrealized income by providing a large gift to survivors. Whole life insurance, however, is significantly more expensive (and complicated!). Although it might be helpful for very high-net-worth individuals or parents with lifelong dependent children, it might not be the most prudent choice for most physicians reading this article.

As always, please consult your fiduciary financial advisor to help determine what is best for your personal situation.

Reference:

- Iervasi K. What is whole life insurance, and how does it work? NerdWallet. https://www.nerdwallet.com/article/insurance/whole-life-insurance. Published Aug. 6, 2024. Accessed June 3, 2025.

For more information:

Chirag P. Shah, MD, MPH, is a soccer and Nordic ski coach who also practices medicine and teaches in Boston. He can be reached at [email protected].

Jayanth Sridhar, MD, is an award-winning podcaster, physician and educator who is chief of ophthalmology at Olive View Medical Center in Los Angeles. He can be reached at [email protected].

Editor’s note: This article is for educational purposes only. Please consult a licensed financial advisor before making any investment decisions.

Disclosure: Shah and Sridhar report receiving and donating royalties as co-authors of Financial Freedom Rx: The Physician’s Guide to Achieving Financial Independence.